SEBI Unveils Life Cycle Funds: Explained

Introduction: SEBI Introduces Life Cycle Funds

In a major overhaul of mutual fund regulations, SEBI has introduced Life Cycle Funds, a new category of open-ended mutual fund schemes designed for long-term, goal-based investing. This move aims to simplify investment decisions, improve transparency, and align mutual fund products with investor time horizons and risk profiles.

What Are Life Cycle Funds?

At their core, Life Cycle Funds are new type of target maturity mutual fund that automatically adjusts asset allocation over time.

Key Features of Life Cycle Funds

- Open-ended mutual fund schemes: Investors can generally enter or exit at any time.

- Target maturity funds: Each fund has a predetermined maturity date tied to a specific time horizon, for example, 5, 10, 15, 20, 25, or 30 years.

- Glide-path based allocations: These funds are structured to start with a relatively higher allocation to equities in initial phase of investment when the maturity date is not near and gradually shift toward safer assets like debt and cash equivalents as the target date approaches.

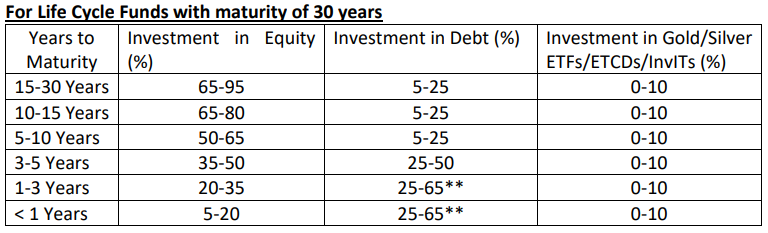

For example, for Life Cycle Funds with maturity of 30 years Years to Maturity, the allocation will look like this:

How Life Cycle Funds Work: Structure and Features

1. Maturity Buckets and Naming

- Life Cycle Funds must include the maturity year in their name, for example, Life Cycle Fund 2045.

- Schemes can have tenures from five years up to 30 years, usually offered in five-year increments (5, 10, 15, etc.).

- Each mutual fund company (AMC) can have up to six Life Cycle Funds active for subscription at any given time.

2. Asset Allocation and Glide Path

The defining feature is a glide path, a dynamic allocation strategy that changes over time:

- In the early years, the fund typically has a higher exposure to equities to benefit from long-term growth potential.

- As the maturity date gets closer, the allocation gradually shifts toward debt and lower-risk instruments to preserve capital.

- These allocations may also include exposure to gold and silver ETFs, InvITs, and ETCDs (Exchange Traded Commodity Derivatives), offering diversification beyond simple equity–debt levels.

This structured shift helps align the portfolio’s risk-reward profile with the investor’s time frame.

3. Exit Loads to Encourage Long-Term Holding

To instill financial discipline and discourage premature withdrawals, SEBI has prescribed a graded exit load regime for Life Cycle Funds:

- 3% if redeemed within the first year

- 2% if redeemed within two years

- 1% if redeemed within three years

Post the third year, no exit load applies unless the scheme’s document specifies otherwise.

4. Fund Mergers Nearing Maturity

As a Life Cycle Fund approaches its maturity (when less than one year remains), it may be merged with another Life Cycle Fund with a close maturity date, but only with the positive consent of unitholders. This provision ensures a smoother transition for investors as part of product lifecycle management.

Phasing Out Solution-Oriented Schemes

Simultaneously with the launch of Life Cycle Funds, SEBI has discontinued the ‘solution-oriented’ mutual fund category, which previously included products like retirement funds and children’s funds. These older schemes will stop accepting fresh subscriptions immediately and are to be merged with other schemes of similar asset allocation and risk profiles, subject to regulatory approval. This shift signals SEBI’s intent to reduce product clutter and ensure that mutual fund offerings remain distinct, transparent, and aligned with clearly defined investor needs.

What This Means for Investors

1. Simplified Goal-Based Investing

Life Cycle Funds provide a structured, hands-off approach that automatically adapts to changing risk profiles over time. Investors seeking a “set-and-forget” portfolio that adjusts itself as a goal date nears may find these products especially beneficial.

2. Enhanced Discipline

The built-in exit loads discourage short-term trading, encouraging investors to stay the course and focus on long-term outcomes.

3. Broader Asset Exposure

By allowing a blend of equities, debt, commodities, and alternative instruments like InvITs, Life Cycle Funds can offer broad diversification under one umbrella.

4. Industry Consolidation and Greater Transparency

The concurrent elimination of solution-oriented categories and tighter classification rules is expected to reduce product duplication in the mutual fund industry and make offerings easier for investors to compare and understand.

Opportunity for MFDs

Life Cycle Funds are not just a new category; they represent a move toward systematic, lifecycle-based investing. For MFDs, this is an opportunity to:

- Deepen goal-based conversations

- Build long-term AUM stability

- Strengthen advisory credibility

Those who understand and communicate this structure effectively can enhance both client trust and business sustainability.

Start your journey with AssetPlus Academy your gateway to becoming a successful mutual fund distributor.

- Get expert-led training for NISM certification

- Learn how to build and scale a long-term, client-centric advisory practice

- Access tools, marketing support, and mentorship to grow your practice

With structured learning, hands-on guidance, and a complete business ecosystem, AssetPlus Academy doesn’t just help you start, it helps you succeed and scale in the evolving mutual fund landscape. Learn More.

Related posts

Become a Mutual Fund Distributor

Build a thriving career as a Mutual Fund Distributor with AssetPlus Academy’s expert-led training and mentorship.