SIP Adoption Is Rising Rapidly. Investor Retention Is The Real Issue

SIPs have grown remarkably in India, and setting up an SIP has never been simpler. Yet the harder question isn’t about ‘how to start a SIP'. It is how to stay invested through full market cycles, long enough for compounding to take effect.

A recent analysis highlighted by Cafemutual points to this quietly, at a time when self-directed investing is widely debated, and financial information is available almost everywhere.

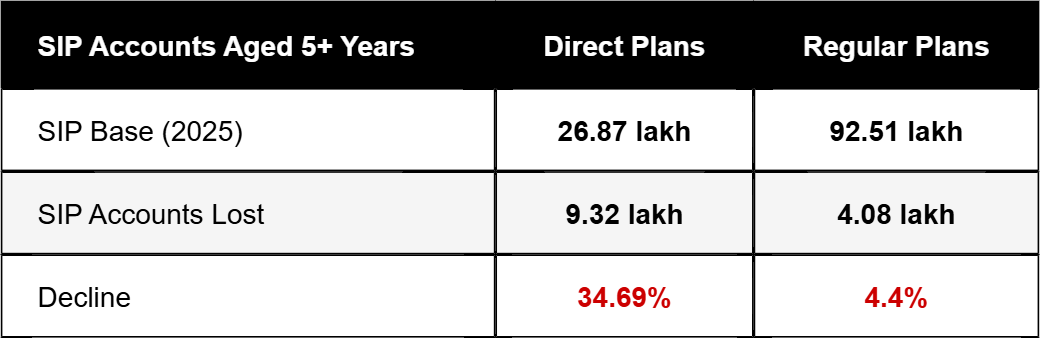

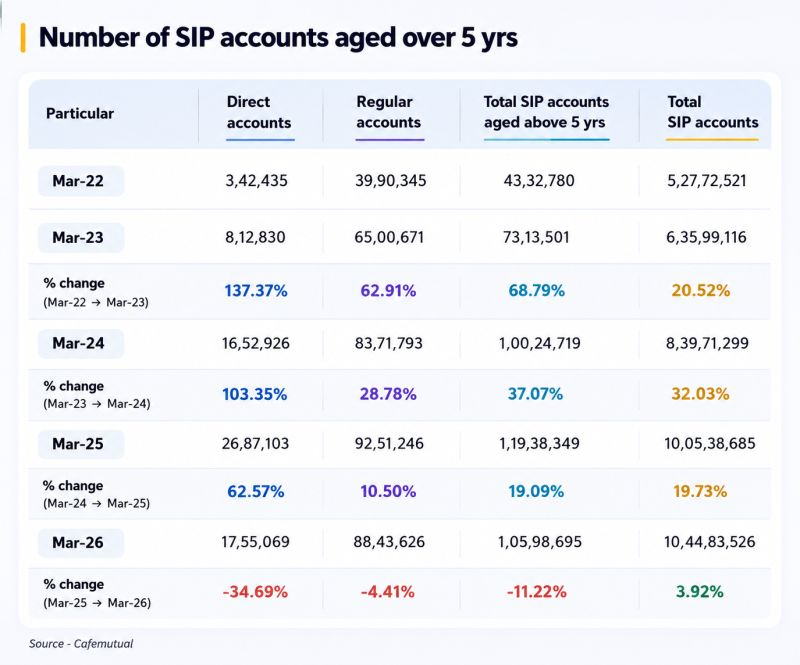

The analysis looked at SIP accounts that had aged more than five years. That pool declined by 11 percent in March 2026. The more telling pattern appeared when the figures were separated into direct and regular plans.

Regular plans saw a modest decline. Direct plans fell by 35 percent, which means close to one in three long-term direct SIPs were discontinued. In absolute terms, direct plans lost 9.32 lakh accounts from a base of 26.87 lakh.

Regular plans lost 4.08 lakh, on a considerably larger base of 92.51 lakh accounts. The pattern suggests that access and awareness, on their own, may not be enough to sustain long-term SIP investing and improve SIP retention in India.

Over recent years, a view has gained ground that guidance matters less now, because information and technology have made investing easy to access and easy to act on.

Information Has Been Democratised. Investor Behaviour Has Not.

Investors today have more financial information than any earlier generation. Fund comparisons, market commentary, return calculators, portfolio analysis, and explainers are all available instantly. Anyone can study a fund, compare options, and begin a SIP within minutes.

This has understandably strengthened the belief that professional guidance is optional. But investing was never only about access to information. The real challenge begins after the SIP is set up as the investor behaviour continues to play a critical role in determining long-term outcomes.

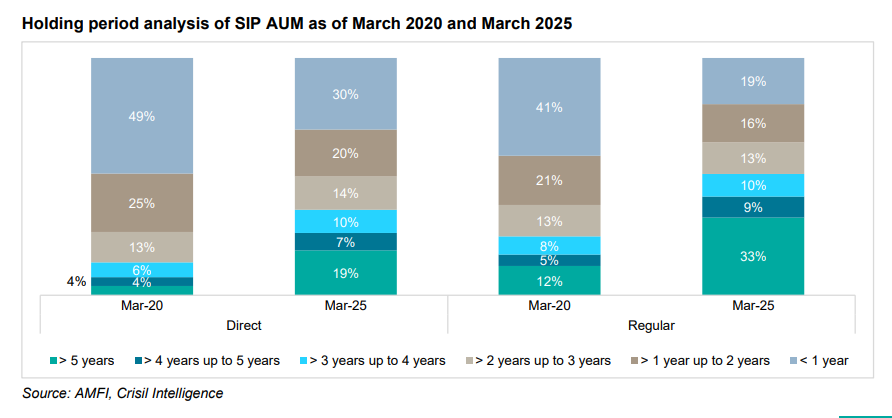

An AMFI comparison of SIP holding periods across direct and regular plans, covering 2020 to 2025, points in the same direction. Investors in regular plans appear less likely to discontinue their SIPs midway than those in direct plans.

This becomes easier to understand when we consider how investing tends to unfold in practice.

Staying invested feels straightforward when markets rise steadily, and portfolios are comfortable. Long-term investing sounds simple in a strong market. The difficulty appears when markets correct sharply, uncertainty rises, the news turns negative, or personal circumstances change. That is when emotion begins to influence decisions.

Not because investors lack information, but because of loss aversion and the instinct to react during volatility. Behavioural research has consistently shown that losses are felt more strongly than equivalent gains, which can lead investors to discontinue their SIPs and interrupt compounding at precisely the wrong time.

Where Guidance Matters Most

This is where the role of an MFD becomes far more meaningful than recommending a fund.

A good MFD understands the investor, not only the portfolio. They consider goals, responsibilities, income stability, risk appetite, and life stage. More importantly, they help investors hold to a plan during the periods when emotion can quietly derail it.

The value of guidance often becomes clear not in the strong years, but in the difficult ones.

Technology and AI can suggest products based on data. They cannot fully provide reassurance, context, accountability, and judgment. A financial journey is rarely a straight line. Every investor encounters uncertainty at some stage, and staying invested through it often shapes whether long-term wealth is created.

Why Staying Invested Matters

The difference between a five-year SIP and a fifteen-year SIP is not linear. It is exponential.

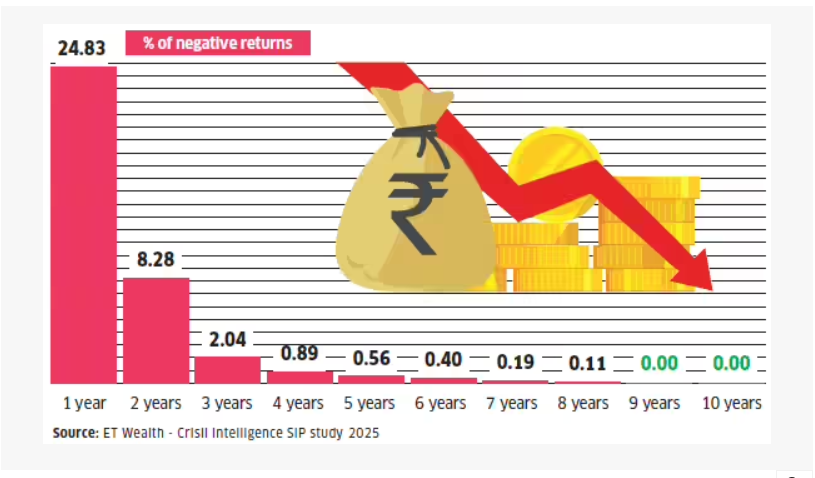

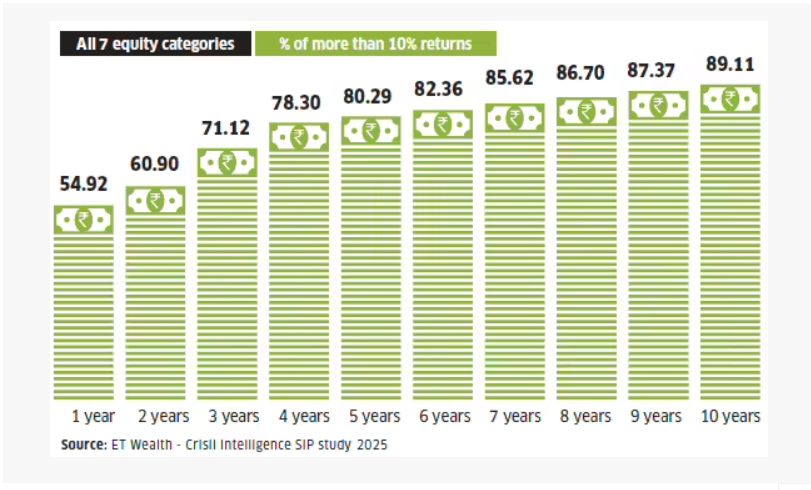

An ET Wealth-Crisil Intelligence SIP study examined performance across equity categories for SIPs running between March 2020 and March 2025, across several rolling periods.

For large-cap SIPs, the probability of negative returns falls sharply as the holding period lengthens.

It took at least five years for these SIPs to reach an 80 percent or higher probability of a strong positive outcome, taken here as a 10 percent return.

The insight matters because it connects investor behaviour in mutual funds directly to investment outcomes. The longer investors remain invested, the stronger their likelihood of stable, meaningful returns through long-term SIP investing. Compounding rewards patience well ahead of perfect timing and reinforces the importance of staying invested in SIPs through different market cycles.

A reasonably good portfolio held steadily for fifteen years can produce far better results than a near-perfect one that is discontinued after a correction. The latest persistence data reflects this clearly. Investors who receive ongoing guidance appear more likely to continue their journey over long periods, highlighting the importance of investor retention in SIP investing.

What This Means For Distributors

None of this is an argument against direct investing or technology-led platforms. The industry could not have reached millions of investors over the past decade without technology making investing accessible.

But accessibility alone cannot resolve mutual fund investor behavioural challenges.

The future is unlikely to be technology replacing MFDs. It is far more likely to be technology supporting MFDs in improving SIP retention, encouraging investors to stay invested in SIPs, and helping investors achieve better long-term outcomes.

For distributors and personal finance professionals, this data reads less as validation and more as a responsibility. The retention gap between guided and unguided investors is not an advantage to celebrate. It is a problem still to be addressed at scale.

For those considering mutual fund distribution as a career, AssetPlus Academy works with you as a growth partner, right from certification to building a sustainable MFD practice. For more information about our courses, visit AssetPlus Academy MFD training programs.

Valueplus Technologies Pvt. Ltd. (AssetPlus)

AMFI Registered MF Distributor | ARN-114376

FAQs

1. Why is investor retention important in SIP investing?

Investor retention is important because the benefits of compounding become more meaningful over longer investment periods. Discontinuing SIPs prematurely can limit long-term wealth creation.

2. Is starting an SIP enough to build wealth?

No. Starting an SIP is only the first step. Staying invested consistently through market cycles is often what determines long-term investment outcomes.

3. What role does investor behaviour play in SIP investing?

Investor behaviour significantly influences outcomes. Decisions driven by market volatility, short-term losses, or emotional reactions often lead to premature exits, which interrupt the power of compounding and hinder wealth creation.

4. How can Mutual Fund Distributors (MFDs) help investors?

MFDs help investors understand risks, align investments with financial goals, provide context during market volatility, and encourage disciplined long-term investing.

5. Can technology replace financial guidance in investing?

Technology can simplify access to investing and provide information, but guidance, reassurance, accountability, and understanding investor needs remain important aspects of long-term investing.

Related posts

.png)

Become a Mutual Fund Distributor

Build a thriving career as a Mutual Fund Distributor with AssetPlus Academy’s expert-led training and mentorship.