.png)

The Rise of the NB-MFD (Non-Bank Mutual Fund Distributor)

The Indian mutual fund industry is undergoing a shift not just in terms of size and reach, but also in the evolving landscape of various players in this sector. For years, banks dominated the distribution matrix, leveraging their sheer strength of a vast branch network, a large base of customers, and a trusted brand position not just in the mutual fund space, but in the entire financial services space.

In the midst of this unquestionable dominance of large banks, Non-Bank Mutual Fund Distributors took a small piece of the pie, reaching individual customers, persisting with their personalised service and long-term trust-based relationships with investors.

However, AMFI’s latest data reveals a different story, a hint of change. But AMFI’s disclosure of top distributors for FY24 vs FY25 reveals something extraordinary: Non-Bank Mutual Fund Distributors (NB-MFDs) are surging ahead.

No, it's not a mere aberration; it’s a trend that could redefine how retail investors engage with mutual funds in India. Let’s unpack the numbers and, more importantly, the reasons behind this tectonic shift.

What the Data Tells Us

In FY24, 2,499 MFDs featured in the top distributor list, including 38 banks. By FY25, the number of MFDs swelled to 3,117, but banks barely moved the needle, inching up to 41. This is more than just growth in numbers; it signals where investor trust and engagement are shifting.

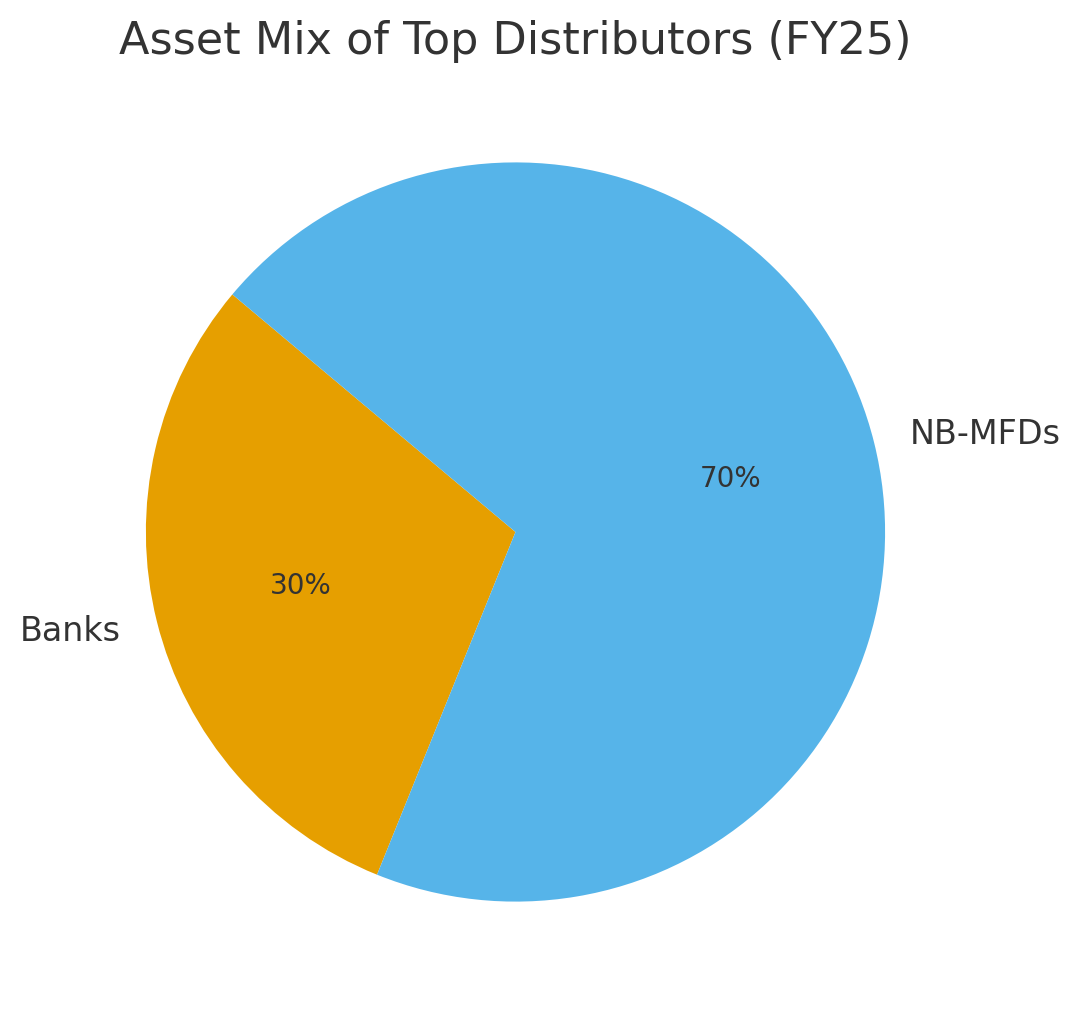

The total AUM managed by top distributors in FY25 touched ₹25 lakh crore, and the split was striking: 70% with NB-MFDs versus 30% with banks.

What’s more, NB-MFDs didn’t just grow in size; they grew faster.

Their year-on-year average AUM growth was an impressive 44%, compared to 30% for banks.

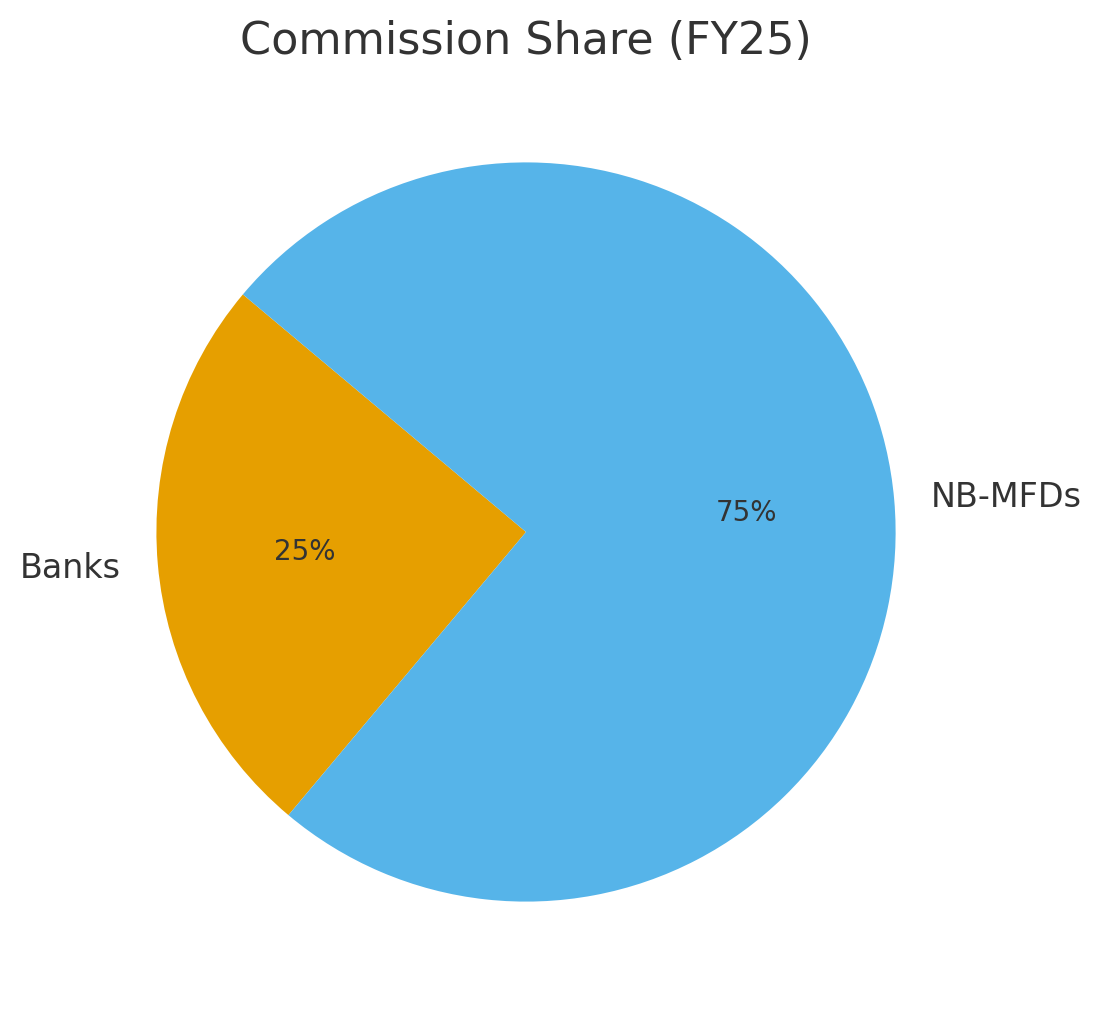

The commission pool tells a similar story; NB-MFDs walked away with 75% of the commissions, leaving banks with just 25%.

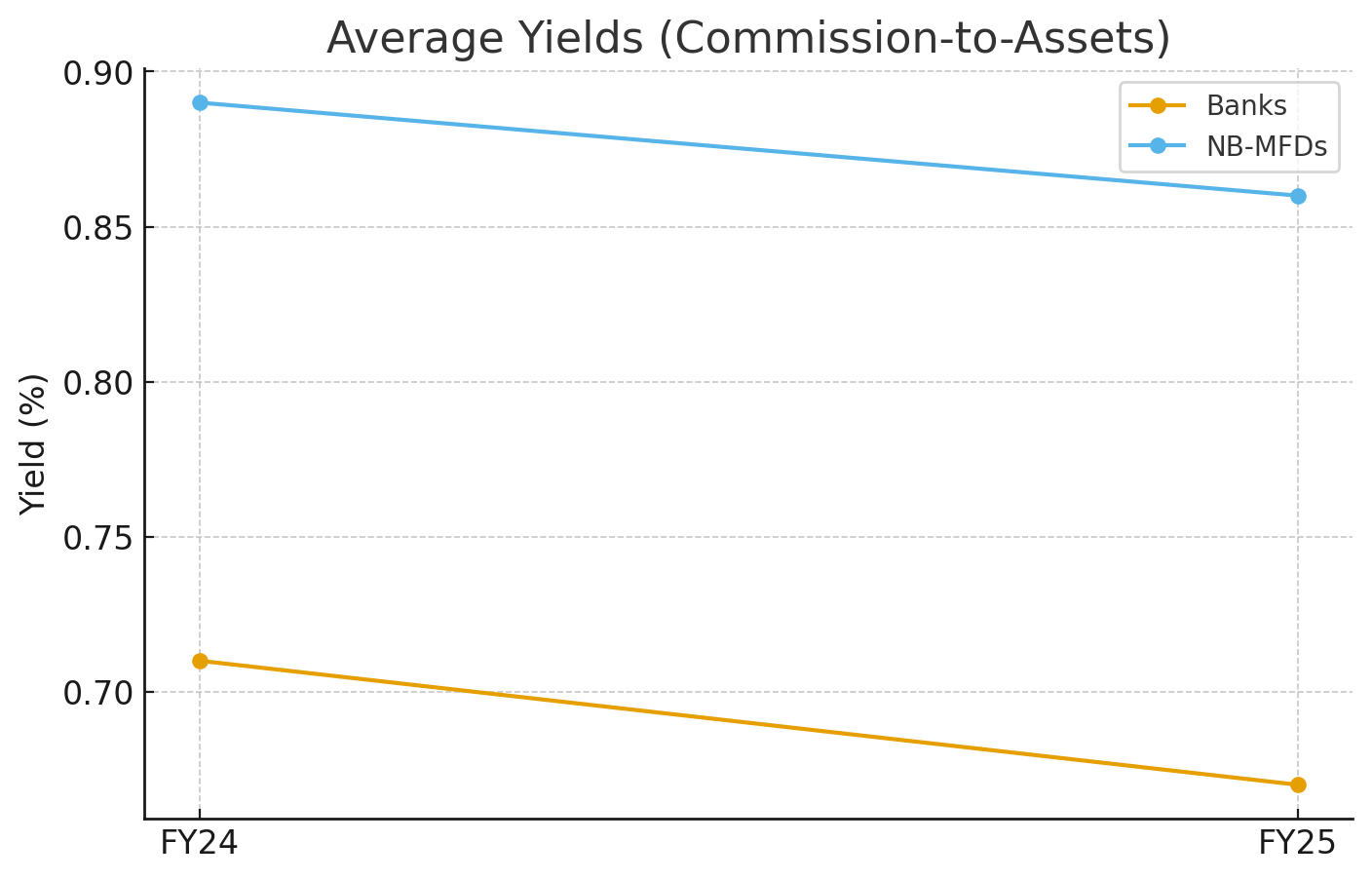

Yield (commission-to-assets): Banks fell from 0.71% → 0.67%, NB-MFDs from 0.89% → 0.86%. Margins are under pressure across the board, but NB-MFDs maintain higher efficiency.

And then there’s the most interesting part: the rise of the smaller NB-MFDs. Those with AUMs below ₹500 crore now earn 23% of total commissions, up from 18% in FY20. In contrast, private banks’ share dropped from 18% to 14%. This democratization of distribution shows that success is no longer limited to giants; even nimble regional players are capturing meaningful share.

These are powerful signals of structural change.

Why NB-MFDs Are Winning

Client Focus & Trust:

Banks often reserve their best financial advice for their ultra-HNI clients, while middle-class investors are nudged toward FDs, ULIPs, or quick-selling NFOs. Relationship managers keep changing, weakening long-term trust.

In contrast, NB-MFDs build sticky relationships, focusing on steady SIP flows. This creates ‘sticky AUM’ that compounds over time.

Core vs Side Business:

For banks, savings, deposits, and lending are the core products; mutual funds are an additional service or value-added product being offered to account holders. Deposit mobilization remains the priority; thus, bank portfolios lean towards FDs or FD-like debt, hybrid or arbitrage mutual funds, and their AUMs end up in a debt-heavy, low-yield mix.

NB-MFDs, meanwhile, offer mutual funds as a core offering and diversify as per the investor profile. They give personal focus to clients and tend to allocate more to equity, the growth driver of long-term wealth.

Equity Advantage:

Non-bank MFDs focus on creating long-term wealth through equity and their portfolios tilt towards active equity funds that boost both client returns and their own commission efficiency.

Entrepreneurial Spirit:

Many seasoned bank relationship managers are breaking away from banks and jumping into entrepreneurship to start independent NB-MFD practices. They bring experience, credibility, and network along with them, thus further adding to the NB-MFD growth engine.

Industry Headwinds

The NB-MFD story also aligns with broader industry trends:

Retailization of Mutual Funds:

SIP inflows are breaking records every year, and NB-MFDs are best positioned to capture this wave. Retail participation has risen from 26% in FY19 to ~28% in FY25 (ET Report). SIP contributions soared from Rs 0.4 Lakh Crore in FY17 to Rs 2.9 lakh Crore in FY25, a 28% CAGR.

NB-MFDs focus on retail investors underserved by mainstream channels, and encourage investors to invest savings into long-term goals through SIPs; most of these investors stick with their SIPs and financial plans under guidance from their MFDs, who focus on building their AUMs rather than chasing upfront sales quotas chased by banks.

Commission Pool Expansion:

FY25 saw mutual fund commission payouts surge ~40% YoY to ₹21,000 crore. The mutual fund distribution continues its shift toward independent/open architecture players compared to banks. The share of national distributors and small agents (AUM below Rs 500 crore) increased marginally on a yearly basis to nearly 75% in FY2025 (63% in FY2019).

Market Tailwinds:

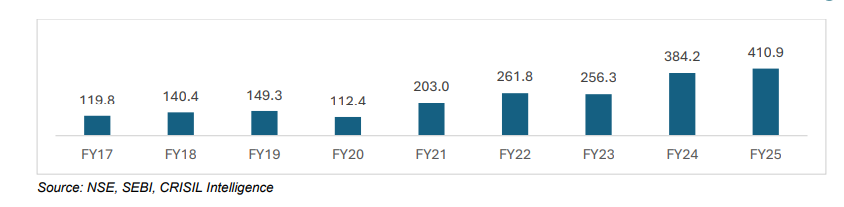

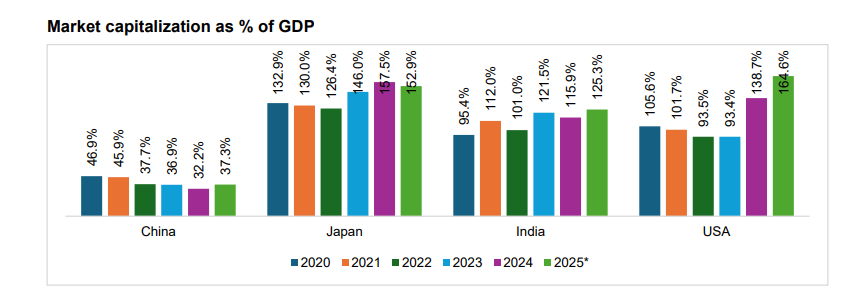

India’s market cap rose to ₹410.9 trillion in March 2025 (up from ₹384.2 trillion a year earlier), The market capitalization of the National Stock Exchange (“NSE”) grew at 13.8% CAGR during Fiscal 2011 to Fiscal 2025. This consistent growth is creating an equity-friendly environment, a positive for the MF industry.

Trend in total market capitalization at the year-end (NSE listed companies) (in ₹ trillion) (ICICI, Crisil Intelligence Report)

Source: World Federation of Exchanges (WFE), IMF, CRISIL MI&A, Data as of Nov 24

Note: * Data is as of Nov’24 as per World Federation of Exchanges (WFE), Market capitalization of Shanghai stock exchange, Japan exchange group, National stock exchange of India, and New York stock exchange has been considered. GDP data taken as per IMF database (April-2025).

Tech + Personalization:

Digitisation has transformed the mutual fund distribution space with many new-age platforms supporting NB-MFDs with digital platforms offering end-to-end digital processes, eliminating operational bottlenecks. MFDs offer instant digital onboarding, investor apps, and dashboards to combine scale with personalized service, an area where banks earlier had an edge; now they are on a level playing field, instead, NB-MFDs are more nimble and swift in delivering services.

AssetPlus is one such platform that not only supports MFDs via a tech platform but also helps them attain knowledge and skills with NISM training, marketing, selling, customer relationship management, social media presence, and more. Reach out to us for a growth partnership to scale your mutual fund distribution business.

Regulatory Push:

SEBI’s pro-investor reforms and AMFI’s investor awareness programs and measures like expense ratio caps have taken mutual fund awareness to remote corners and positioned mutual funds as a secure and well-regulated investment avenue, allaying the fear of the unknown. Agile NB-MFDs have adapted to this market awareness faster than banks.

Structural Penetration Gap:

Mutual fund penetration in India remains low compared to global peers. For example, reports suggest Indian MF AUM-to-GDP is 19% vs 140% in the U.S. There are only 5.5 crore unique mutual fund investors in the country, making almost 130 crore population a target market waiting for the right guidance and awareness. This means there is significant room for growth, especially outside metros/top-tier cities, making a fertile ground for NB-MFDs.

Margin Pressure & Efficiency Tradeoffs:

Because commission yields are compressing for both banks and NB-MFDs, the ones with cost control, scale, and retention will be more efficient and thrive. NB-MFDs, by virtue of being small-scale and nimble, can manage costs and cross-sell, bundle services, and offer solutions with mutual funds + insurance/loans tie-ins to diversify revenue.

Niche and local knowledge ground:

The fact that NB-MFDs with < ₹500 crore AUM now command almost 23% of MF distribution commission, these regional and niche players may be more agile, trusted locally, and better equipped to serve the often-ignored, underpenetrated markets.

What This Means for the Future

The data is undeniable: NB-MFDs are no longer underdogs. They’re reshaping how mutual funds reach India’s growing investor class. Their dominance in equity allocation, SIP-driven retail flows, and commission share reflects a deeper transformation, one where trust, specialization, and agility beat legacy and infrastructure.

Looking ahead, NB-MFDs will need to prepare for margin pressures as yields compress. But with scale, efficiency, and tech adoption, they’re well-positioned to thrive. The rise of smaller NB-MFDs also hints at a future where distribution is more democratized and regionally driven, rather than bank-led.

What This Means for the Industry

The distribution power is shifting away from banks, and this is no small feat.

NB-MFDs are proving that trust, service, and focus can outcompete brand, infrastructure, and legacy.

The retail-adoption of mutual funds through SIPs and middle-class participation is the true story, and NB-MFDs are best placed to ride this wave.

The Final Word

The mutual fund distribution business in India is no longer just about size and legacy. It’s about focus, agility, and client-first orientation.

NB-MFDs aren’t just participating in the race; they are reshaping the industry dynamics itself one SIP at a time, slowly and steadily.

And if the current trends continue, the future of mutual fund distribution will be in the hands of smaller NB-MFDs, given the scope and potential beyond metro cities.

Become a Successful Mutual Fund Distributor with AssetPlus Academy. Join the 12-Day expert-led live online training and ace the NISM V-A Mutual Fund Certification Examination. Enroll Now.

Related posts

Become a Mutual Fund Distributor

Build a thriving career as a Mutual Fund Distributor with AssetPlus Academy’s expert-led training and mentorship.